By Adam Bernstein, Investment Analyst

It’s worth restating the opening line from our previous blog: What a difference a few weeks can make.

In this piece, we focus on how recent events affecting the “Mag 7” have strengthened our view that the S&P 500 can no longer be relied upon as the only portfolio growth engine. At the start of 2026, market participants were largely bullish on AI and broader corporate performance. This was only compounded by excitement regarding anticipated SpaceX, Open AI, and Anthropic IPOs.

Then February arrived, and the narrative rapidly shifted.

We believe that advisors should consider re-positioning client portfolios to capture upside from capital rotation towards industrials, energy, and materials, and reduce the risk of any S&P 500 drawdowns.

AI Enthusiasm Tempers, AI Fears Grow

In early February, Anthropic rolled out Claude Opus 4.6 which has ‘agent team’ capabilities and the ability to handle significantly more complex requirements than prior versions.1 Later that month, it publicly announced that it did not support the U.S. Department of War using its technology for mass surveillance and autonomous weapons.2 The Pentagon subsequently switched to OpenAI, which led many users to switch to Claude, pushing it to the top spot in Apple’s App Store.

Meanwhile, Citrini Research released a memo “from the future” exploring a scenario where AI’s expansion leads to rising unemployment, especially in white-collar jobs. “It should have been clear all along that a single GPU cluster in North Dakota generating the output previously attributed to 10,000 white-collar workers in midtown Manhattan is more economic pandemic than economic panacea.”3 While rebuttals argue for AI’s potential to create new industries and new jobs, software stocks reacted with a knee-jerk sell-off.

AI’s capabilities are exciting, but they are hugely transformative and disruptive, and very likely more so than prior technological revolutions. While we can’t predict the future, the large companies developing much of the technology are likely to see diminishing margins. Jeff Currie of Carlyle argued back in November 2025 that the tech sector’s current capex cycle is analogous to that undertaken by energy companies in the shale revolution. “Big Tech AI is now producing a physical commodity with a supply and demand balance just like an energy company…. It’s perfectly fine for AI to be a commodity, of course: just don’t be surprised when industry multiples get priced like one.”4

Big Tech and War in the Middle East

As we discussed in our prior blog, February also brought the start of U.S.-Israeli strikes on Iran. This conflict is obviously consequential in its own right, with major risks to human lives from both direct warfare as well as indirect impacts from energy markets, and subsequently, food systems. However, for this piece we focus on the risks to Big Tech, and therefore the S&P 500.

It’s no secret the U.S. is experiencing domestic grid constraints as well as local pushback for datacenter builds. It’s less well understood that the Middle East is a key region for datacenter expansion. Relatively low costs for power and land, in addition to favorable digital infrastructure, among other attributes, were seen to position the region as “a data centre [sic] powerhouse, with capacity… projected to triple, from 1GW in 2025 to 3.3GW over the next five years.”5

However, in March, Amazon AWS datacenters in the UAE and Bahrain suffered damage to buildings and infrastructure from drone strikes. AWS expressed the risk of “prolonged disruptions.”6 At of the time of this writing, there is no sign of an end to the strikes, only serving to increase the risk for local data centers and the infrastructure and energy supplies they rely on.7 How will the Mag 7 address these concerns given existing and planned facilities in the region?

What Can Advisors Do?

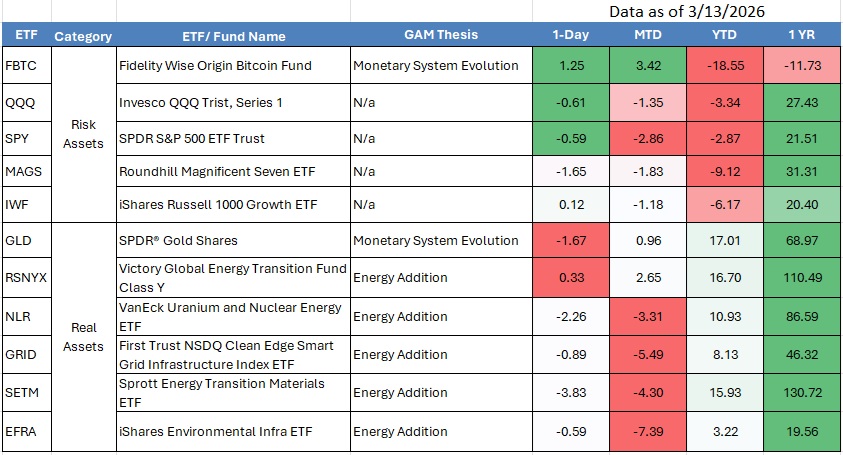

As shared in prior commentaries, we are a thematic investor focusing on global systems-level shifts. Via our core theses - Energy Addition, Climate Adaptation, and Monetary System Evolution - we’ve been managing our Mag 7 risk while increasing exposure to energy, metals, minerals, water, and gold. We believe that our approach is better suited to our current climate of uncertainty than passive indexing. While nobody can predict the future, it is possible to manage risks, especially those stemming from concentration in passive portfolios. Below we are resharing the visual from our last blog that compares performance for risk assets and real assets.

We agree with J.P. Morgan Asset Management’s 2026 Long-Term Capital Market Assumptions that “macro and market conditions look very different than they did in the post-GFC period” and that this is a “new era for active investing.”8 In building our models and suite of investment strategies, we have been diligencing and working with skilled active managers for several years. We welcome sharing how their deep expertise and specific approaches can be combined in managed models to support the needs of your practice and your clients.

If you’d like to learn more about how we approach risk and opportunity through a thematic lens, please feel free to book a 30-minute call with me.

This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and the understanding that the recipient has sufficient knowledge and experience to be able to understand and make their own evaluation of the proposals and services described herein, any risks associated therewith and any related legal, tax, accounting or other material considerations. To the extent that the reader has any questions regarding the applicability of any specific issue discussed above to their specific portfolio or situation, prospective investors are encouraged to contact Gitterman Asset Management or consult with the professional advisor of their choosing.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by Gitterman Asset Management. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Gitterman Asset Management or any other person. While such sources are believed to be reliable, Gitterman Asset Management does not assume any responsibility for the accuracy or completeness of such information. Gitterman Asset Management does not undertake any obligation to update the information contained herein as of any future date.

This presentation is confidential and is intended only for the person to whom it has been directly provided.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Gitterman Asset Management is a dba of Perigon Wealth Management, LLC ("Perigon"), a registered investment advisor registered with the U.S. Securities and Exchange Commission.

[1] https://techcrunch.com/2026/02/05/anthropic-releases-opus-4-6-with-new-agent-teams/

[2] https://www.anthropic.com/news/statement-department-of-war

[3] https://www.citriniresearch.com/p/2028gic

[4] https://www.carlyle.com/carlyle-compass/ai-compute-market-price-analysis

[5] https://www.pwc.com/m1/en/media-centre/articles/unlocking-the-data-centre-opportunity-in-the-middle-east.html

[6] https://www.bloomberg.com/news/articles/2026-03-03/drone-strikes-damage-amazon-data-centers-in-the-uae-and-bahrain

[7] https://www.bloomberg.com/news/articles/2026-03-13/trump-warns-iran-to-watch-what-happens-as-war-hits-two-week-mark

[8] “2026Long-Term Capital Market Assumptions: 30th Annual Edition”. 2025. J.P. MorganAsset Management

Get in touch

If you have questions, or think our solutions are right for you, please reach out using the form below. We will respond as soon as possible to continue the conversation.

379 Thornall Street, 2nd Floor

Edison, NJ 08837

(848) 248-4405