By Adam Bernstein, Investment Analyst

What a difference a few weeks can make.

At the start of 2026, the investment consensus was fairly positive and unusually aligned. Equity valuations were viewed as reasonable given strong earnings, massive capital expenditures tied to AI were applauded, fiscal policy was deemed supportive, and we had expectations for a more accommodative Federal Reserve. The prevailing narrative was straightforward: investors should remain fully allocated to risk assets.

However, beneath the surface, growth was slowing: consumer spending had decelerated meaningfully, business investment outside of AI-linked sectors was soft, and manufacturing activity was largely stagnant. Alongside these the labor market was beginning to deteriorate.

As economic weaknesses started to become more visible in the data via declining payrolls, stalling job creation, and sticky inflation, the U.S. launched Operation Epic Fury. The economy was already in a more fragile position with less room for policy adjustment, and now a war was underway.

The Strait of Hormuz

We now face major disruption to global energy markets that may foreshadow significant human consequences beyond the direct impacts currently facing the inhabitants of the Middle East. In 2024, the Strait of Hormuz was the thoroughfare for roughly 20 million barrels of oil per day, representing one-fifth of global petroleum consumption and more than a quarter of all international seaborne oil trade.1 The Strait also transports LNG and other refined petrochemical products, as well as fertilizer feedstocks, and critical industrial outputs such as sulfuric acid and helium. Disruption to these flows reverberates through electricity markets, plastic production, the mining industry, airline ticket costs, and ultimately, food systems and many manufactured goods.

As of this writing (March 18, 2026) we see varied country and market responses. For example:

When supplies contract, stockpiling and hoarding behaviors rise. Carlyle notes, “In 1979, a 4–5% physical shortfall triggered precautionary hoarding that doubled the effective demand impact. The same dynamic is now operating at far greater scale. China has suspended petroleum product exports. Every major importer is securing supply simultaneously. We estimate that precautionary demand could be 2-3 million b/d over the next 3-6 months. The physical disruption is the trigger; the behavioral response is the multiplier.”5

The Outlook

There are many unknowns as we write this. How long will the situation persist? How long will it take to bring flows back to normal even if the Strait returns to prior activity levels?

Even with a near-term return to something like “normal,” many commentators are suggesting that this is a paradigm-shifting event. Moreover, the lag effects alluded to above will continue to move through global systems and markets over the coming months. The magnitude of these depends on the persistence of the war.

We believe that the events of 2026 will accelerate the shifts we’ve been experiencing since the supply chain shocks of COVID. Countries are increasingly focusing on re-shoring, on-shoring, and energy security, while overall trust is waning. The Strait of Hormuz forces us to confront where global capacity is more limited than it appears. The U.S. may be a net exporter of oil, but we overestimate the fungibility of a barrel. The diagram below from S&P Global is an excellent illustration of the wide variety of crude output. Global refineries are generally set up to process specific crude types and cannot easily shift if supply in one region suddenly goes offline. Therefore, the global impacts can be more complex than they first seem.

In this new landscape, security of supply matters more than marginal cost. This means that physical capacity matters more than financial engineering. For debt-ridden Western countries that have diminished ownership or control over physical supply, this is an especially challenging situation, but also a clue to where capital will flow.

Energy, critical minerals, and other inputs will likely become more expensive. This will cause inflation throughout the broader economic system. This may spur innovation in material and energy use over time, but there is no simple, immediate substitution in many industries today. Airlines may reduce flights, but routes that keep flying will come with higher ticket prices. Manufacturers and energy companies will keep producing where possible, but expect to see costs passed through to consumers. Turning back to recent commentary from Carlyle, oil is now “more irreplaceable in function. The remaining barrels are the ones for which no substitute exists: petrochemical feedstocks, aviation fuel, grid balancing, fertilizers. Remove them, and you do not get demand destruction — you get production shutdowns. We believe the world is more vulnerable to an oil shock today than it was in 1973, not less.”6

Increasing Commodities Allocations

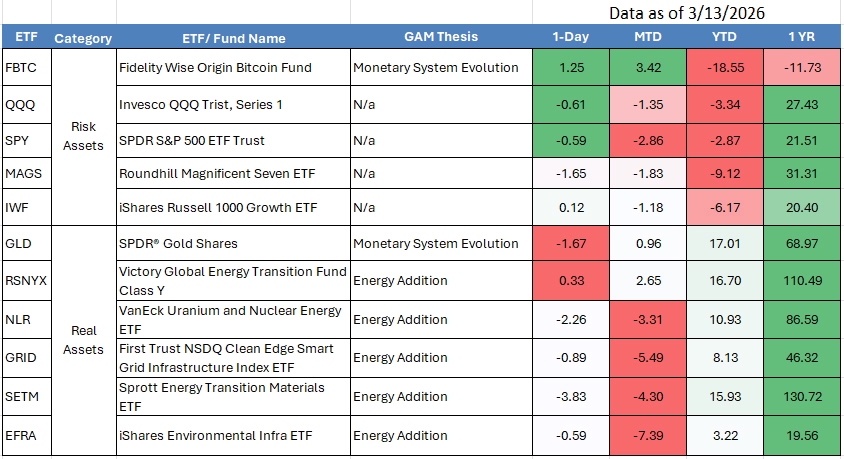

Performance this year has been strongest in assets tied to the physical economy. Commodities have moved higher, gold has rallied and uranium and nuclear-related equities have outperformed. Infrastructure and resource-linked exposures have also generated positive returns. At the same time, many of the assets that defined the consensus entering the year — large-cap growth, speculative technology, and crypto — have lagged.

We are now seeing some retracing within some of these commodities and sectors, and may see more. However, our long-term view is that commodity sectors will do better than Big Tech (more to follow on this in a separate blog). In addition, future price action may have direct lines back to the Strait of Hormuz for some parts of the commodity complex. Qatar is one of the world’s biggest producers of sulfur, the key feedstock for sulfuric acid, as a byproduct of natural gas. Sulfuric acid is a key input for the fertilizer industry, but also for resource extraction. “In metals processing, it is used mainly in leaching, where crushed ore is treated with acid so valuable metals such as copper, nickel, cobalt and uranium can be dissolved and then separated, purified and recovered.”7

Pursuant to our core theses - Energy Addition, Climate Adaptation, and Monetary System Evolution - we’ve been increasing exposure to energy, metals, minerals, water, and gold. We believe that our thematic approach is better suited to our current climate of uncertainty than the traditional 60/40 portfolio. While nobody can predict the future, we believe that the actively managed strategies that we include within our models are well positioned to help manage risks and capture upside from geopolitics, as well as sectoral and regional rotations.

If you’d like to learn more about how we approach risk and opportunity through a thematic lens, please feel free to book a 30-minute call with me.

This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and the understanding that the recipient has sufficient knowledge and experience to be able to understand and make their own evaluation of the proposals and services described herein, any risks associated therewith and any related legal, tax, accounting or other material considerations. To the extent that the reader has any questions regarding the applicability of any specific issue discussed above to their specific portfolio or situation, prospective investors are encouraged to contact Gitterman Asset Management or consult with the professional advisor of their choosing.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by Gitterman Asset Management. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Gitterman Asset Management or any other person. While such sources are believed to be reliable, Gitterman Asset Management does not assume any responsibility for the accuracy or completeness of such information. Gitterman Asset Management does not undertake any obligation to update the information contained herein as of any future date.

This presentation is confidential and is intended only for the person to whom it has been directly provided.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Gitterman Asset Management is a dba of Perigon Wealth Management, LLC ("Perigon"), a registered investment advisor registered with the U.S. Securities and Exchange Commission.

[1] https://www.eia.gov/todayinenergy/detail.php?id=65504

[2] https://fortune.com/2026/03/11/iran-war-fuel-crisis-asia-work-from-home-closed-schools-price-caps/

[3] https://www.reuters.com/world/middle-east/uae-temporarily-closes-its-airspace-an-exceptional-precautionary-measure-2026-03-17/

[4] https://www.bloomberg.com/news/articles/2026-03-18/philippines-in-talks-with-china-and-russia-on-fertilizer-supply

[5] https://www.carlyle.com/global-insights/a-crude-awakening

[6] https://www.carlyle.com/global-insights/a-crude-awakening

[7] https://theoregongroup.substack.com/p/strait-of-hormuz-is-chokepoint-for?

Get in touch

If you have questions, or think our solutions are right for you, please reach out using the form below. We will respond as soon as possible to continue the conversation.

379 Thornall Street, 2nd Floor

Edison, NJ 08837

(848) 248-4405