In our final edition of the Summer Series, we turn to emerging markets. For the RBC Emerging Markets Equity team, ESG is a critical component of their investment philosophy and process. This includes a detailed assessment of climate-related risks and opportunities as part of the stock selection process, company engagement activities, and top-down thematic research.

Because emerging markets are disproportionately affected by both the physical risks and financial consequences of climate change, and the substantial deficits in social infrastructure and investment have been exacerbated by the COVID-19 pandemic, RBC believes Green Infrastructure is a multi-decade growth story.

In their most recent thought leadership piece, Green Infrastructure, RBC identifies three key drivers shaping the trend: global warming, health implications exacerbated by climate change, and the responsiveness of governments seeking economic solutions in pursuit of global supremacy in effectively addressing adaptation and physical climate risks.

To that last point, public concern has forced climate change onto governments’ political agendas. As a result, Green Infrastructure is likely to provide a source of economic growth for many countries around the world as countries consider and announce climate-related spending packages. President Biden announced that the intended $2.5tn infrastructure plan is likely to focus on Green Infrastructure and decarbonization. China committed to a net zero carbon target by 2060 and has invested heavily in electric vehicles and renewable sources of energy. Similar announcements from other governments globally are anticipated.

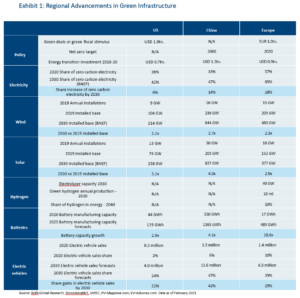

Exhibit 1 shows the differences in policy between the U.S., Europe and China that underpin the Green Infrastructure theme.

RBC suggests that the best way to play the Green Infrastructure theme is to begin with the sources of energy consumption most responsible for man-made greenhouse gases. According to the International Energy Agency, 73% of CO2 emissions are attributed to energy consumption, specifically electricity, heating, and transportation, as noted in Exhibit 2.

Within these sectors, renewable energy is set to be the fastest growing energy source over the next two decades, driven primarily by solar and wind power. Transport accounts for 25% of global CO2 emissions, mainly because the sector relies so heavily on oil. New modes of transport – such as electric passenger vehicles, buses, and trains – should make the transport sector cleaner, assuming renewables are used to generate the underlying electricity. As the cost of batteries falls there will be increasing price parity between EV and internal combustion engine (ICE) vehicles, which RBC believes could mark the inflection point for EV sales.

One of the most attractive parts of the EV value chain is the component manufacturers segment. These high return businesses have strong pricing power and are not exposed to the heavy capex cycle and competitive environment that are found in other parts of the value chain (Exhibit 3).

Exhibit 3: ICE versus EV Manufacturer’s Suggested Retail Price by components

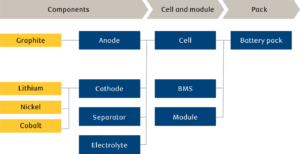

Delving deeper into the EV value chain of battery manufacturers, there are multiple parts of the value chain required to produce battery packs that offer economic opportunities. (Exhibit 4)

Exhibit 4: Battery pack components

Source: Macquarie Research. Data as of December 2020.

In terms of the cost breakdown, currently the cell accounts for about 76% of the total cost of the battery pack with the module cost estimated to be around 10%.1

Significant economies of scale in battery cell production mean that the sector is largely dominated by several large players. In 2014, the top three battery manufacturers represented 56% of the total and that increased to 70% in 2020. According to RBC, “South Korean battery manufacturers have the highest market share with the scope to increase that share and are the most technologically advanced with good OEM diversification.” This explains their slight preference towards South Korean cell producers.

These are but a few of the Green Infrastructure themes and opportunities presented by RBC thought leadership. You can read the full report here.

Get in touch

If you have questions, or think our solutions are right for you, please reach out using the form below. We will respond as soon as possible to continue the conversation.

379 Thornall Street, 6th Floor

Edison, NJ 08837

(848) 248-4405