Last week, at the final FOMC meeting of 2022, the Federal Reserve raised rates by 0.50% (to a range of 4.25% – 4.50%) as expected while unexpectedly increasing its dot plot forecast of where it believes rates will be in 2023 and beyond. Notably, the expectation for the Fed funds rate at the end of 2023 was raised to 5.1%, a big increase from the 4.6% expected at the September meeting. The Fed also revised its estimate for 2023 GDP growth down to just 0.5% and increased its inflation expectations.1 In the press conference following the meeting, Fed Chairman Jerome Powell clarified that the dot plot implied no rate cuts at all in 2023, throwing cold water on those hoping for an imminent pivot.

The initial market reaction was disbelief. The Fed’s surprising hawkishness was enough to halt the stock market rally that had begun in October but was not enough to trigger a serious selloff or a repricing of forward rate expectations. In fact, Treasury rates were flat or fell slightly from the time of the meeting through the end of the week. The skepticism was understandable. November CPI did show encouraging signs of slowing, coming in at 7.1% compared to 7.7% in October.2 Layoffs from the tech and financial sectors have started to hit the headlines. In a normal market environment, the Fed skeptics would be correct to question such a hawkish path but, as has been the theme of this decade, nothing about this situation is normal.

Out of everything that makes this time different, the labor market is the most crucial to understand. In a normal rate hiking cycle, high inflation causes the Fed to raise interest rates to slow demand, which reduces inflation. Higher interest rates also increase costs to businesses and ultimately result in rising unemployment and recession. The Fed’s challenge is to manage the tradeoff between keeping inflation in check while minimizing the pain inflicted on regular people. But now the Fed finds itself in a unique position. It is hiking rates against the backdrop of a structural labor shortage that is both exerting upward pressure on inflation (via rising wages) and providing the Fed more leeway to raise rates before the impact on workers becomes politically untenable.

Powell explicitly addressed the labor shortage in last week’s press conference. He described it as structural rather than cyclical and estimated that around 3.5 million workers are “missing” from the labor force, attributing the gap to early retirements, reduced migration and half a million excess deaths among workers since the start of the pandemic. We agree with all of the above but would add Long Covid disability, the opioid crisis, and childcare issues to the list of labor shortage causes that are unlikely to resolve in the short-term.

Whatever the drivers of the labor shortage, what are the implications for Fed policy and, by extension, the market and economic outlook for next year? Quite simply, the Fed can (and may be forced to) raise rates to a higher level and keep them there for longer than it has in the past before seeing a negative impact on workers. If a recession begins, corporate layoffs may not be at the same scale as in prior recessions as companies have been struggling to hire workers for a couple of years. There is no glut of boom time workers to lay off, aside from the tech sector, since over hiring hasn’t been possible. Managers who learned from experience may hoard the workers they do have while cutting costs elsewhere.

Unlike prior hiking cycles, the brunt of the pain of rate hikes looks like it will fall on corporate profit margins and risk asset valuations rather than on average Americans, at least until the labor market normalizes. We don’t expect a pivot from the Fed until after the unemployment rate begins to increase and expect equity returns to be weak or negative for some time past that point. We are also preparing for another leg down in the bond market as interest rates price in the Fed’s new dot plot and corporate bonds begin to price in rising default risk from a near-certain 2023 recession. We are maintaining a very defensive stance in our portfolios, which are underweight equity and overweight cash with a short duration high quality bond allocation.

Finally, Some Good News: A Breakthrough in Nuclear Fusion

What happened?

On December 5th, U.S. scientists at the National Ignition Facility in California generated a nuclear fusion reaction that created a net energy gain, an important breakthrough in the search for a clean and affordable energy future. The experimental result is a massive nuclear energy breakthrough in a century-long quest to harness fusion energy.

What is nuclear fusion?

Nuclear energy as we know it today comes from fission reactions, which split atoms to release energy. Nuclear fusion is the process of fusing two atoms into a single atom, which releases a tremendous amount of energy. Nuclear fusion is the reaction that fuels the stars in our universe, including our sun.

Why is it important?

Ever since the theory of nuclear fusion was understood in the 1930s, scientists and engineers have been trying to recreate and harness it. If nuclear fusion can be replicated at an industrial scale, it could provide virtually limitless clean, safe, and affordable energy to meet the world’s energy demand. Fusing atoms together in a controlled way releases nearly four million times more energy than a chemical reaction such as the burning of coal, oil or gas and four times as much as nuclear fission reactions. Fusion has the potential to provide the kind of baseload energy needed to provide electricity to our cities and our industries.

Investment implications:

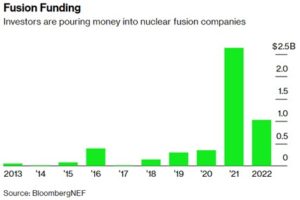

There are about 35 companies currently working on some form of nuclear fusion. The U.S. government has invested in nuclear fusion programs since the 1950s, but all the money has gone towards national labs, universities, and the Primary International Research Project in France (ITER). This year marks the first time that the US government has invested directly in private sector fusion energy companies.

Notable recent raises for companies seeking to commercialize fusion include Commonwealth Fusion Systems, TAE Technologies Inc. and Helion Energy Inc. Other fusion companies that have landed significant backing include Marvel Fusion GmbH, General Fusion, Tokamak Energy Ltd., and Zap Energy Inc.

Perspective:

“Whereas a giant pile of carbon-spewing coal might generate electricity for a matter of minutes, the same quantity of fusion fuel could run a power plant for years–with no carbon dioxide emissions.” – NPR

Fusion offers an exciting new opportunity in energy generation. If commercialization can be achieved, this form of energy would solve the intermittent issues with renewable energy sources such as solar and wind and provide a base load energy source like hydrocarbons and nuclear energy without the health, safety, environmental, and raw material supply chain issues. But there is still a way to go. About 300 megajoules of energy were needed to fire the laser that was used in the fusion experiment, while the reaction showed a net gain of only about 1.1 megajoules (barely enough energy to boil a teakettle 3 times).

The private fusion industry has seen almost $5 billion in investment, according to the industry trade group, the Fusion Industry Association, and more than half of that has been since the second quarter of 2021. It took 11 years and billions of dollars to set up and successfully execute this one laser test. So, we still have a long road ahead of us before commercialization can be reached. Using history as a guide, it took the world 37 years to split the atom, from that start of atomic research in 1895, until the first atom was split in 1932 at a laboratory in the UK. It then took another 28 years for the world to commercialize this process for use within the energy grid, with the first nuclear power plants going operational in 1957. While the promise of fusion to solve our most pressing energy and climate issues is unmatched, the uncertain timeline means that we must continue to invest in renewables and other emission reduction technologies.

Get in touch

If you have questions, or think our solutions are right for you, please reach out using the form below. We will respond as soon as possible to continue the conversation.

379 Thornall Street, 6th Floor

Edison, NJ 08837

(848) 248-4405